View all

Web DevelopmentMobile Development UX/UI DesignStaff Augmentation CTO as a ServiceDedicated TeamLow-Code Development15 Fintech Startup Ideas Worth Building in 2026

Trends

Fintech

Jun. 26, 2026

18 min to read

Table of Contents

How to Evaluate a FinTech Startup Idea Before You Build

AI-Powered FinTech Startup Ideas

Payments and Banking FinTech Startup Ideas

WealthTech and Investment FinTech Startup Ideas

InsurTech and RegTech FinTech Startup Ideas

FinTech Startup Ideas for Emerging Markets

How to Validate and Build Your FinTech Startup Idea

The global fintech market may exceed $460+ billion by 2026, thus creating numerous business opportunities. However, the competition remains high. Many fintech startups struggle not because their product ideas are weak, but because the market is saturated or the regulatory model is underestimated. Building a successful product today requires not just a modern UI but also airtight compliance and sustainable unit economics.

If you are looking for viable fintech startup ideas, you are in the right place. In this guide, we bypass generic concepts and break down 15 high-potential fintech opportunities. They reflect the most actionable fintech startup trends of the year. For every idea, we provide an honest evaluation of the market size, technical complexity, monetization model, and regulatory risks—so you can make an informed decision, rather than guessing what to build next.

How to Evaluate a FinTech Startup Idea Before You Build

When founders come to us to scope their fintech startup ideas, they often focus on the features they want to offer to the end consumers. But a feature is not a business, even if it aligns with 2026 fintech startup trends. To differentiate a "cool concept" from a viable, buildable business model, you need a rigorous evaluation framework. Founders routinely miscalculate by overestimating their technological differentiation while underestimating compliance costs.

To help you assess the ideas below, we apply a consistent four-pillar framework to every concept:

| Evaluation Criterion | What It Means for Your Startup | Why It Matters |

| Market Opportunity | The market size, growth trajectory, and specific underserved gaps. | Determines whether the idea can attract VC funding or reach profitability as an MVP. |

| Technical Complexity | The estimated timeline to build an MVP and the required technology stack. | Directly affects your initial burn rate and determines the type of engineering team you need. A Banking-as-a-Service (BaaS)-partnered MVP typically costs between $50,000 and $150,000 and takes 3–6 months to launch. |

| Monetization Model | The exact mechanics of how the product generates revenue (e.g., SaaS, interchange, AUM). | Defines unit economics. For example, standard interchange revenue yields roughly 1% to 3% per transaction, meaning high transaction volume is essential. |

| Regulatory Risk | The compliance burdens, necessary licenses, and legal hurdles in your target jurisdiction. | Compliance is one of the biggest risks for fintech products before launch. Knowing this upfront saves a lot of money. Securing an independent banking or multi-state transmitter license can easily cost $500,000+ and take 12–24 months. |

From our experience building FinTech products, we see that the most expensive mistake founders make is writing code before understanding the licensing requirements. An attractive application will be useless if you cannot legally process transactions in your target market. So, always validate regulatory feasibility first.

Validating a fintech concept right now?

Before you commit to a tech stack, let’s evaluate your idea together and map out a realistic MVP timeline.

AI-Powered FinTech Startup Ideas

Artificial intelligence is a fundamental new layer of capability built on top of existing financial infrastructure. The most promising AI fintech startup ideas focus on efficiency and personalization. If you are exploring fintech startup ideas 2026, AI is the sector where technical execution allows startups to compete with legacy banks. At the same time, they do not need to carry their massive operational overhead.

AI-Powered Credit Scoring and Alternative Lending

Traditional credit scoring systems often fail to assess thin-file or unbanked users. So you can launch an ML-driven platform to assess applicants' creditworthiness. It should use alternative data points. Still, some sort of information is highly sensitive. For example, it could include mobile phone usage patterns, utility payment histories, and behavioral data. That is why you should integrate explicit user consent and data protection measures. Rely on secure, opt-in data sharing to accurately assess risk while fully respecting user privacy.

There is a massive unmet demand for such services across Sub-Saharan Africa, Southeast Asia, and Latin America. Here, the middle class is growing, but thin-file borrowers dominate. You can earn from the interest margin on originated loans, B2B SaaS licensing for traditional banks, or API fees for BNPL platforms.

The technical complexity of such projects is medium to high. They require robust ML modeling and seamless API partnerships with alternative data providers, such as telcos and utilities. You will also need a highly secure data pipeline. Also, you may face challenges such as biases in ML models and regulatory scrutiny. For example, compliance with the EU AI Act requires models to be transparent and explainable. Regulatory review of algorithms is performed to ensure compliance with these rules.

From our experience, the biggest technical bottleneck here isn't training the ML model. The more challenging task is building resilient API gateways that can process messy, unstructured data from local telcos and utility providers without timing out.

AI Financial Assistant / Copilot

An LLM-based personal financial assistant goes beyond passive dashboards. It analyzes spending with advanced tools and predicts upcoming cash flow challenges. Such an AI-driven assistant may provide actionable advice via a real-time conversational interface. You can offer a freemium and a premium subscription to your customers at approximately $10–20/month. Also, you can earn affiliate revenue from highly targeted financial product recommendations.

AI copilots are especially attractive for high-income millennials and Gen Z who suffer from subscription fatigue and complex, fragmented finances. In a response, they are seeking proactive wealth management.

The technical complexity of building an AI financial assistant is medium. This project requires integration with modern LLM APIs. Also, you will need secure Personal Financial Management (PFM) data aggregation via Plaid or TrueLayer, as well as a reliable notification layer.

The main risk for launching an AI financial copilot is getting user trust. People are highly sensitive to AI hallucinations when it comes to their money. That is why strict data privacy, including PII masking, is mandatory.

We’ve seen that users quickly abandon AI copilots if there’s even a slight latency in fetching their bank data. Building a robust caching layer alongside your LLM integration is critical to maintaining a truly real-time, conversational feel.

AI-Driven Fraud Detection as a Service

Enterprise fraud solutions like Featurespace or Feedzai are incredibly powerful for protecting companies' assets. Still, their $200k+ annual price tags can leave mid-market companies unprotected. So you can launch a B2B SaaS API that offers real-time fraud detection and account takeover prevention may meet growing market demand. To cover the market gap, these services should be priced and packaged for mid-market e-commerce, neobanks, and regional lending platforms. The SMB and mid-market segment is underserved. So, if you want to find a serious customer base, offer SMBs protection against AI-generated fraud schemes.

The general monetization pattern for this idea is the usage-based pricing per transaction. Also, you can set up a base platform fee plus a percentage of the funds recovered or saved.

The technical complexity is high, as you will need sub-second real-time ML scoring, graph-network databases for anomaly detection, and continuous model retraining pipelines.

Key risks include positive rates. If your model declines too many legitimate transactions, you directly damage your client's conversion rate and revenue. From our experience, false positives are disrupting startups in this niche. We recommend running the MVP in "shadow mode" first. You need to benchmark the algorithm's decisions against historical transaction data. Only then can you let it actively block payments.

Payments and Banking FinTech Startup Ideas

Moving money faster, cheaper, and across borders remains one of the most attractive fintech startup ideas. The best fintech startup ideas 2026 in this space focus on embedding financial services into existing workflows rather than building standalone consumer apps. For a deeper dive into the underlying technology, check out our article on Innovations in Payment Systems.

Embedded Finance Platform for Vertical SaaS

You can start integrating your financial products, such as payment processing, lending, or bespoke insurance, into vertical-specific SaaS platforms. For example, they can be useful for real estate agencies, dental clinics, or software for auto dealerships. Nowadays, vertical SaaS is experiencing a huge demand. Adding financial services allows these platforms to multiply their Average Revenue Per User (ARPU) by capturing the flow of funds. In response, you will earn your revenue from interchange fees, deposit interest margins, and loan origination fees.

The technical complexity of such an idea is medium. It requires integration with BaaS providers or embedded finance platforms such as Unit or Stripe Treasury. You may choose other providers, depending on the region. This will allow building a robust compliance layer and creating a seamless UX within the host platform. Still, you will incur counterparty BaaS risk. The highly publicized collapse of Synapse in 2024 stranded millions of users and caused severe operational disruptions for dependent fintech platforms. That is why choosing a robust infrastructure partner is very important.

We’ve seen that platforms often struggle with payment state management when relying on third-party BaaS APIs. Implementing an event-driven architecture early on saves months of painful refactoring when transaction volumes inevitably spike.

Cross-Border Payroll for Remote Teams

Enterprise giants such as Deel and Remote dominate the top end of the market. However, their pricing is often prohibitive for smaller businesses. There is a clear gap in pricing and usability for lean startups and agencies that hire employees from different countries. They need to pay contractors in 30+ countries without massive platform fees. That is why you can launch a highly automated platform for managing payroll, multi-currency conversions, and tax compliance. It should be designed for mid-market companies with distributed global teams.

Revenue from such a project can come from a per-employee, monthly SaaS fee of approximately $20–$50. Also, you may benefit from FX conversion margins and from upselling premium HR/compliance features.

The technical complexity of managing cross-border payroll is high. Such a platform will require complex multi-currency payment rails. You will need to automate local labor law compliance logic and implement sophisticated FX hedging to protect margins. You may face regulatory fragmentation because you will need to consider distinct labor laws and tax codes. Also, you will need to comply with stringent AML/KYC regulations for international payouts across numerous jurisdictions.

From our experience, handling FX volatility is often harder than the payroll logic itself. Startups that succeed here build dedicated microservices strictly for real-time currency hedging and liquidity management.

Real-Time B2B Payments and Cash Flow Management

Astonishingly, up to 82% of small-business failures are tied to poor cash flow management, not a lack of profitability. B2B payments are extremely archaic for today’s dynamic market. Small businesses desperately need to bridge the gap between sending invoices and receiving cash. That is why you can initiate a platform that replaces slow, batch-processed ACH payments with real-time payment rails such as FedNow or RTP. It should be combined with intelligent, predictive cash flow forecasting. To get revenue from this idea, you can introduce a tiered SaaS subscription and premium analytics. You can also earn a per-transaction fee for instant settlements.

The technical complexity for such a platform is medium. It requires deep integration with ERPs/accounting software (QuickBooks, NetSuite), FedNow/RTP APIs, and predictive ML for cash flow analytics. When starting the project, you may face ecosystem fragmentation and slow adoption of new payment rails by legacy payer organizations.

We’ve seen that legacy ERP systems have notoriously brittle APIs. Your engineering team should spend the majority of their time building custom, fault-tolerant middleware to seamlessly sync your platform with tools like NetSuite or QuickBooks.

WealthTech and Investment FinTech Startup Ideas

The democratization of wealth management is one of the main opportunities for new fintech startup ideas. They are driven by fintech startup trends toward fractionalization and algorithmic management. The goal is to give retail investors access to asset classes previously reserved for institutional players. Secure asset management is a key to modern WealthTech.

Fractional Real Estate Investment Platform

You can use blockchain and tokenization technologies to allow retail investors to buy fractional ownership of commercial or residential real estate. The starting price could be as low as just $100. Companies that exploit this idea, such as RealT and Lofty, already exist. Still, global market penetration remains incredibly low, especially when you consider markets outside the US.

Owners of such platforms can take an asset management fee of 1–2% annually. To their revenue streams, they can add transaction fees on secondary market trades and listing fees for property developers.

The technical complexity for such investment platforms is high. They require EVM-compatible smart contracts, strict KYC/AML gateways, and a secure custody solution. Under the hood, a tokenized real estate platform shares many architectural patterns with digital asset exchanges. We have a strong technical foundation in this Web3 space. We built the secure custody and fiat-to-crypto architecture for Myntkaup and engineered the frontend for MuesliSwap, a decentralized exchange. Real estate tokenization introduces its own unique domain challenges. Still, our experience with smart contract execution, digital wallet security, and making complex on-chain data intuitive for retail users allows us to navigate these overlapping technical requirements effectively.

The main risk of such projects is severe regulatory scrutiny. These assets are classified as securities, not utility tokens. They require compliance with SEC Regulation A+ or Regulation CF, or local equivalents, plus the ongoing challenge of providing secondary-market liquidity.

Robo-Advisory for Underserved Segments

You can launch an automated, hyper-personalized investment management app. It should target Gen Z and millennials with a low initial capital requirement. New brands need to differentiate themselves from giants such as Betterment and Wealthfront. They will catch the market opportunity by focusing on micro-investing, conversational AI interfaces, and highly specific value-based portfolios. So, such an app may target thematic and ESG (Environmental, Social, Governance) portfolios.

The technical complexity for this fintech project is medium. This kind of app relies on portfolio optimization algorithms. They need integrations with broker-dealer APIs, such as Alpaca, and real-time automated rebalancing.

With this investment management app, you can earn an Assets Under Management (AUM) fee of 0.25–0.50%, plus a flat subscription for premium features and tax-loss harvesting. Still, you may face high customer acquisition cost (CAC) relative to the low initial lifetime value (LTV) of micro-investors.

From our experience, the backend calculations for fractional shares and automated rebalancing are highly prone to rounding errors. Using precise decimal libraries and immutable event ledgers from the beginning is necessary for a WealthTech product.

SMB Treasury Management Platform

Enterprise companies use costly software such as Kyriba or SAP TRM. Still, businesses doing $1M–$50M in revenue leave their cash sitting idle in checking accounts, losing value to inflation. For such clients, you can offer an automated treasury management system that actively sweeps idle SMB cash into low-risk yield-generating assets. An example of such an idea is a low-risk instrument such as a money market fund. This innovative system should integrate features such as FX hedging and liquidity forecasting.

Such a platform can bridge the gap between business checking accounts and expensive enterprise treasury software. You can earn AUM fees on the yield generated, a SaaS subscription, and spreads on FX conversions.

The technical complexity for this platform is medium to high. It requires integration with brokerage APIs, dynamic sweep logic, and highly accurate cash flow predictions to ensure the business always maintains operational liquidity. Still, you may face market volatility and counterparty risk. If there are settlement delays, SMBs will not be able to access their operational cash immediately. In such a case, the platform will not perform its primary function.

We’ve seen that latency in dynamic cash sweeps can cost businesses real money or leave them without operational liquidity. Your infrastructure must be optimized for asynchronous processing to safely capture yield.

InsurTech and RegTech FinTech Startup Ideas

InsurTech and RegTech may look less consumer-facing, but these fintech startup ideas can solve expensive operational problems. The fusion of AI fintech startup ideas with compliance is creating highly defensible, sticky B2B products.

Usage-Based Insurance (UBI) Platform

Consumers are frustrated when they must pay high premiums to subsidize riskier policyholders. That is why businesses may move away from static premiums toward dynamic insurance pricing based on real-time behavior. For example, you can use vehicle telematics for auto insurance, or IoT/wearables for health and life insurance. For such projects, you can introduce premium margins, B2B data licensing, and white-labeling the technology to legacy insurance carriers.

The technical complexity for the UBI platform is medium to high. It requires massive IoT data-ingestion pipelines, real-time actuarial pricing engines, and a Managing General Agent (MGA) structure. Remember that since underpricing risk is fatal, you will need accurate actuarial modeling. Also, you will face heavy data protection concerns regarding tracking user behavior.

We’ve seen that ingesting continuous streams from IoT devices or telematics creates massive database bloat. Implementing time-series databases specifically tuned for high-write workloads is a structural lesson many InsurTechs learn the hard way.

AI-Powered RegTech for AML/KYC Compliance

Regulatory fines for AML violations are sharply increasing. That is why mid-sized banks and neobanks desperately need tools to reduce the manual headcount required for compliance. You can launch a B2B SaaS platform that automates AML and KYC workflows using NLP capabilities. This technology will be useful for parsing corporate documents. It can graph databases to uncover ultimate beneficial ownership (UBO) and conduct a real-time sanctions screening. For this project, you can use multiple revenue streams, such as charging per API check, offering tiered monthly SaaS plans, or creating custom contracts for enterprise clients.

The technical complexity for RegTech platforms is high. You will need deep NLP training on legal documents, intricate graph database architecture, and zero-latency integration with global sanctions lists (OFAC, EU). A main risk is that the startup could face regulatory issues if the software fails to flag a sanctioned entity, allowing it to bypass controls. Deciding who is responsible — the SaaS vendor or the financial institution — is still a complicated legal question.

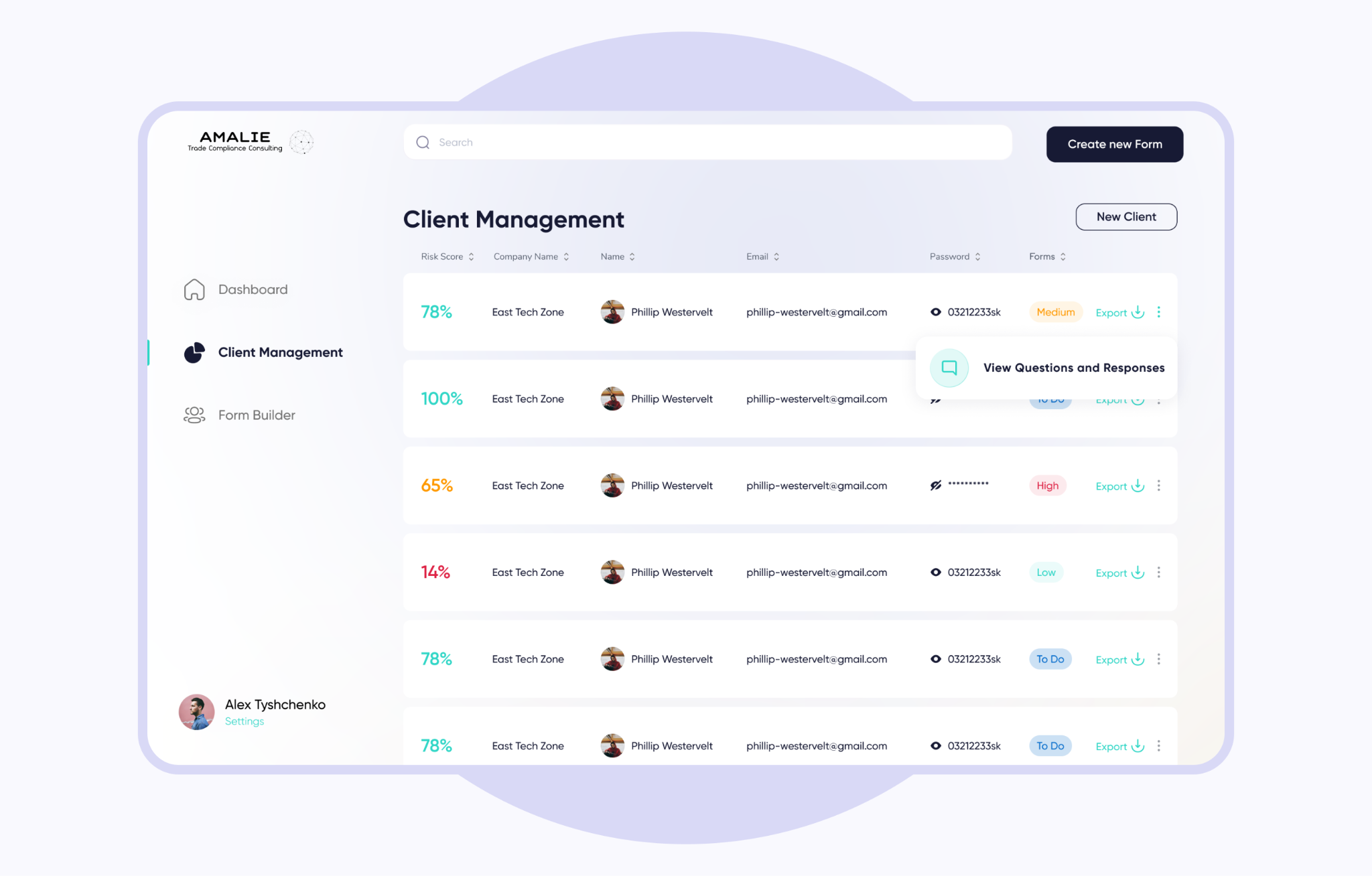

The backbone of any RegTech startup is an efficient, automated risk-scoring pipeline. For instance, we developed Amalie, a custom risk assessment platform for a US-based trade compliance consulting firm. By automating complex client data collection and dynamic risk calculations, we helped them eliminate manual compliance overhead.

Automated Claims Processing Infrastructure

Processing a claim manually often costs an insurer more than the claim's actual value. Automating this task saves millions in operating expenses. So, you may launch an API-first platform that uses computer vision and LLMs to perform certain claims processing tasks. Its main purpose will be to verify, process, and pay out standardized micro-insurance claims instantly. For example, this could be flight delays, minor auto damage, or pet insurance.

To earn the money, you can introduce a flat fee per claim processed on this platform. Also, the revenue can come from a percentage of the insurer's operational cost savings.

The technical complexity of this infrastructure is high. Such a platform requires highly trained computer vision models. They are essential for damage assessment and secure integration with real-time payout rails.

When launching the project, you may face fraud amplification. If bad actors reverse-engineer the automated approval logic, they can drain funds at scale before a human intervenes.

We’ve seen that the hardest part of an automated claims product isn't the AI or computer vision. It's the secure orchestration layer that connects the automated approval directly to legacy banking payout rails without introducing new fraud vectors.

FinTech Startup Ideas for Emerging Markets

The highest growth potential over the next decade lies not in the saturated markets of the US or the EU. The most explosive fintech startup trends are found in regions with low traditional banking penetration but massive mobile adoption. Let's look at the best fintech startup ideas in India for 2026 and beyond.

Micro-Credit Layer on Top of UPI (India)

India's digital public infrastructure processes billions of transactions each month. You can benefit from building short-term, low-value credit facilities on top of India's Unified Payments Interface (UPI). By using the RBI-approved “Credit Line on UPI” framework, startups can offer instant, low-value checkout credit to the MSME (Micro, Small, and Medium Enterprises) sector or thin-file retail consumers. Offering embedded credit on ubiquitous UPI rails lowers customer acquisition costs. At the same time, you may reach a massive unbanked or underbanked middle class.

By launching such a service, you can earn origination fees, interest on the utilized credit, and revenue-sharing agreements with partner banks. Note that standard UPI transactions mandate zero Merchant Discount Rate (MDR). However, credit-linked UPI transactions allow for interchange fees. This makes monetizing through merchants highly sensitive due to systemic resistance to payment fees. That is why you may face high default rates among thin-file borrowers, intense merchant pushback against credit-related fees, and strict compliance with the RBI's evolving digital lending guidelines.

The technical complexity of this initiative is medium. The UPI infrastructure is robust. The complexity lies in the real-time alternative risk assessment algorithms and seamlessly integrating with the core banking systems of partner banks that actively issue the credit lines.

From our experience, relying solely on a single sponsor bank for UPI access is a point of failure. We advise architecting for multi-bank redundancy to ensure 99.99% uptime during peak loads.

B2B Financial Infrastructure for Super-Apps (Southeast Asia)

Following the models of Grab and GoPay, regional apps with large user bases in SEA seek to monetize through financial services. At the same time, they want to achieve this aim without building a bank from scratch. So, you may provide a modular API infrastructure that non-financial consumer apps for ride-hailing or e-commerce can integrate to become regional super-apps. This financial infrastructure can handle lending, insurance, wealth management, and other operations.

With such a project, you can charge platform licensing fees and share revenue from financial products sold through the APIs. Still, you may face intense competition from established regional tech giants. Also, you will operate in shifting regulatory environments across distinct SEA countries.

The technical complexity of this B2B infrastructure is high. It must be ready to handle huge transaction volumes and regional currency conversions. Developers need to deal with fragmented regulatory environments across Indonesia, Vietnam, and the Philippines.

From our experience, scaling microservices across multiple SEA countries requires a deeply localized approach to data residency. You cannot simply deploy a single centralized cloud cluster and expect to remain compliant across national borders.

Mobile Money Lending and Remittance APIs (Sub-Saharan Africa)

Mobile money serves as the banking system in much of Africa. You can set up an interoperability layer that lies above fragmented mobile money networks such as M-Pesa or MTN MoMo. This layer unlocks trapped value and offers excellent profit opportunities. It may be needed for cross-network remittances, bill payments, and micro-insurance distribution. You can charge microtransaction fees on cross-network transfers and API access fees for international remittance providers.

The technical complexity of such APIs is medium to high. You will be dealing with legacy telco APIs, inconsistent uptime, and the need to secure USSD-based transactions.

Businesses starting such projects are risking over-reliance on telco monopolies. The latter can arbitrarily change API access rules or pricing structures overnight.

We’ve seen that when integrating with legacy telco infrastructure, API documentation is rarely accurate, and timeouts are frequent. To prevent lost transactions, you need to build highly robust error-handling and automated reconciliation scripts.

Neobanking and SME Merchant Ecosystems (Latin America)

Latin America remains the hottest fintech region of 2025–2026. To illustrate the scale, Nubank surpassed 110 million customers in Brazil alone by early 2026, serving roughly 61% of the adult population. Despite these massive B2C successes, a huge gap remains in providing affordable working capital and digital payment tools to the region's vast informal SME economy.

So, you can build a dual-sided financial ecosystem that combines a consumer-facing digital wallet with B2B merchant acquiring tools (similar to the models of Mercado Pago or Clip). By providing small businesses with accessible point-of-sale (POS) solutions and linking them directly to a consumer neobanking app, startups can create a highly lucrative, closed-loop financial system.

You can earn on merchant discount rates (MDR) for payment processing, interchange fees on card transactions, and high-margin interest from short-term consumer and SME loans.

The technical complexity of such a project is high. It requires engineering a dual-sided platform, a B2C app, and a B2B merchant dashboard. You will need to integrate it deeply with local instant payment rails such as Brazil's PIX or Mexico's SPEI and deploy ML models for credit scoring using merchant transaction data.

Key risks include high currency volatility across different LATAM markets. Your business will depend on unpredictable political shifts that impact regulatory frameworks and on intense competition from established regional super-apps.

We’ve seen that integrating with instant payment rails like PIX requires an architecture capable of extreme concurrency. A standard monolithic backend will inevitably buckle under the pressure of regional peak shopping events.

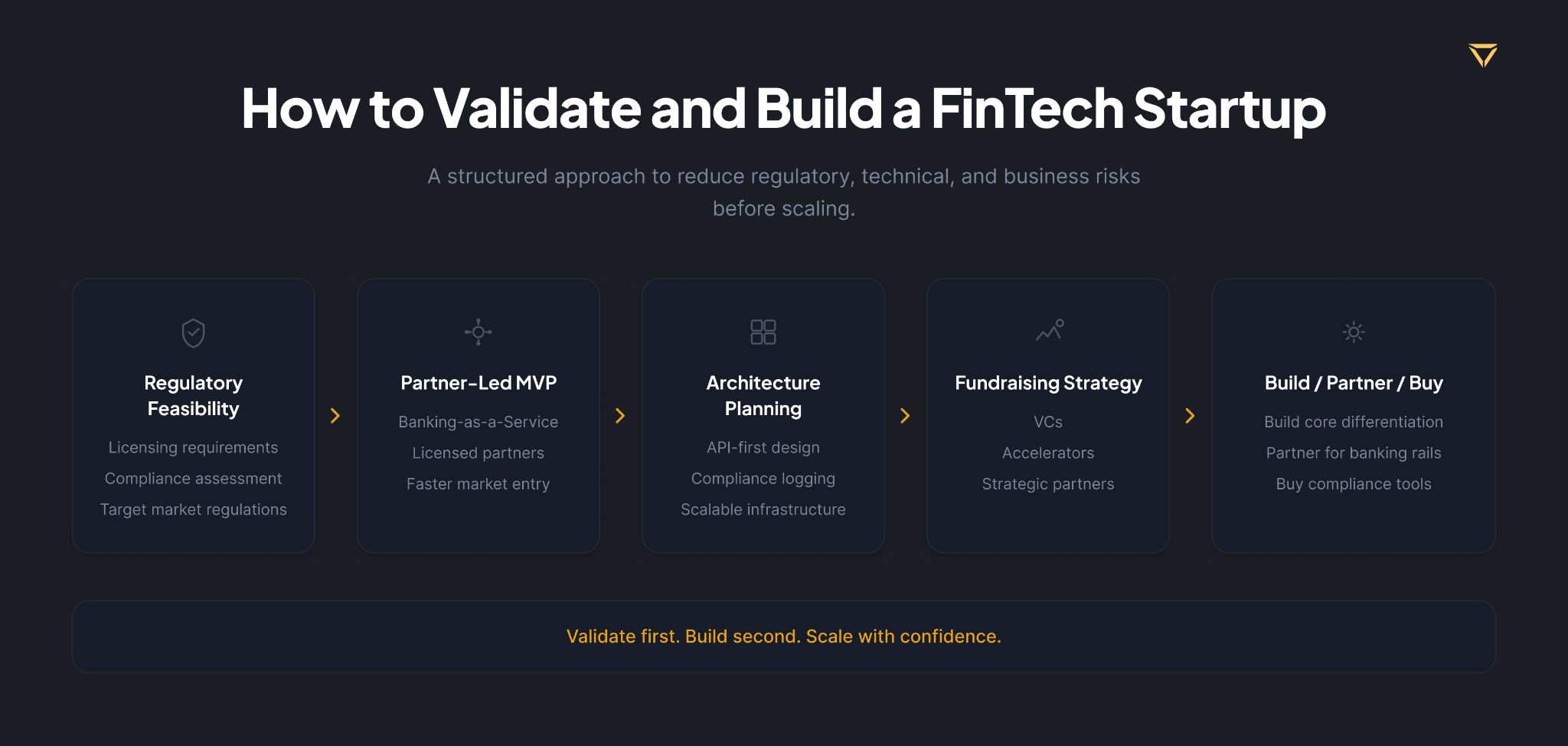

How to Validate and Build Your FinTech Startup Idea

Having a great idea is only the start of the journey. Executing it, given current fintech startup trends, requires a meticulous, de-risked approach. If you are assessing these fintech startup ideas, follow this blueprint to get to market without burning your runway.

Step 1 — Regulatory feasibility first: Before writing code, map out your licensing requirements. It would be a mistake to build a product for 6 months only to discover you need a transmitter license that takes 2 years and $500,000 to acquire. Talk to a compliance lawyer at the beginning of the project. Budget $20-50k for initial regulatory consultation; expect 4-8 weeks for licensing feasibility assessment.

Step 2 — Partnership-first MVP: You rarely need your own banking license to launch. Use the help of BaaS providers, broker-dealer partnerships, or MGA structures. They will allow you to rent compliance. This can help validate product-market fit faster.

Step 3 — Technical architecture choices that matter early: Implement an event-driven architecture. Adopt an API-first design for future BaaS integrations and build compliance logging natively. Retrofitting compliance into an app later is much more difficult.

Building for scale and high traffic is critical in financial services. For example, our team has worked with the Finance.ua project on a staff augmentation model. Our team members contributed to frontend architecture and data-heavy product flows for a platform with 5M+ monthly visitors.

Step 4 — Fundraising landscape 2026: Bootstrapping a regulated fintech is very hard. Target specialized VCs, such as a16z FinTech or Ribbit Capital, or accelerators like YC and Plug and Play. Beyond just capital, they offer the industry credibility and warm introductions needed to help you secure essential banking partnerships.

Step 5 — Build vs. Partner vs. Buy: Don’t build commodities from scratch. Working with fintech founders, we typically advise: Buy your KYC/AML stack (Sumsub and Onfido have proven themselves in our Amalie project). Partner for BaaS rails (we've integrated with Unit, Stripe Treasury). Build only your proprietary risk algorithm, your UX, and the parts that defend your moat.

Have a fintech idea and not sure where to start?

The Stubbs.pro team has built payment platforms, lending products, and compliance infrastructure for startups and scale-ups across Europe.

FAQs

1. What are the most promising fintech startup ideas in 2026?

What are the most promising fintech startup ideas in 2026?

You can discover the high potential in AI-powered credit scoring for underserved markets and embedded finance within vertical SaaS. Try to benefit from B2B real-time payments, addressing cash flow management, automated RegTech for AML/KYC, and usage-based insurance. They either lower the costs of existing operations or capture markets that traditional finance has ignored.

2. How much does it cost to build a fintech startup MVP?

How much does it cost to build a fintech startup MVP?

The cost depends on regulatory complexity and infrastructure choices. A baseline fintech MVP built on a BaaS partnership typically costs $50,000 to $150,000 and takes 3 to 6 months to launch. With such a solution, you can avoid the need for an independent financial license. Platforms that require complex compliance layers or independent licenses start at $200,000+. They take 9 – 18 months to develop. Compliance and legal fees are usually your biggest variable.

3. Do I need a financial license to start a fintech company?

Do I need a financial license to start a fintech company?

You don’t necessarily need a financial license. Many fintech MVPs are partnering with a licensed sponsor bank or a BaaS provider. This gives them the regulatory cover needed to validate their product. However, if you want to scale or enter high-risk areas, you may need your own licenses or a stronger regulated partner model.

4. What are the best fintech startup ideas for India in 2026?

What are the best fintech startup ideas for India in 2026?

India offers great opportunities due to its robust UPI infrastructure and expanding middle class. The best ideas include building micro-credit layers on top of UPI for thin-file borrowers, mobile-first insurance distribution platforms, and SMB invoicing tools with integrated alternative credit scoring. The RBI's regulatory sandbox supports experimentation in regulated fintech use cases.

5. What AI fintech startup ideas have the most potential?

What AI fintech startup ideas have the most potential?

The highest potential lies in using AI to eliminate expensive human operations or to analyze unstructured data. Startups may focus on predictive cash flow modeling for SMBs, automated regulatory compliance (RegTech), or dynamic, behavior-based pricing for insurance. The best AI fintech concepts change unit economics, allowing a lean startup to operate with the efficiency of a traditional bank.

6. What fintech business models are most sustainable?

What fintech business models are most sustainable?

The most sustainable models include B2B SaaS solutions with recurring revenue, such as RegTech or treasury management tools. The second option is an API infrastructure that earns fees based on transaction volume. And the third is embedded finance products that fit into daily business routines. On the other hand, standalone personal finance apps for consumers often struggle with high user turnover and making money.

7. How long does it take to build a fintech product?

How long does it take to build a fintech product?

Creating a working MVP with a BaaS partner usually takes 3 to 6 months. Maybe you want a platform with more advanced features, such as multi-currency support, custom analytics, and a special compliance setup. This project can take 9 to 18 months. Products that need their own regulated infrastructure or direct licenses often take 18 to 36 months. Legal and compliance checks can also lengthen the process.

Jun. 26, 2026

18 min to read